Is C&RT selling BWML to pay off £13m loan?

March 2018 - Canal & River Trust has decided to throw in the towel with its BWML marina subsidiary and sell it. This will allow one of BWML’s larger competitors, or a new competitor, to expand massively by acquiring 18 marinas and over 3,000 berths. Allan Richards delves into BWML’s history.

BWML came into being in 2004 after the trade accused British Waterways of anti competitive practices with regard to the operation of its larger marinas. British Waterways Marinas Ltd as it was then, was set up as an arms length subsidiarity company with BW providing both directors and equity. BW and C&RT have always claimed that it treats BWML no differently from any other marina operator.

In 2006, BW decided to encourage private building of new marinas to cope with a shortfall in berths and expected increase in demand. It set up a New Marina Unit and published an ‘Inland Marina Investment Guide’. The guide stated ‘During the past two years,British Waterways subsidiary marina company (BWML) has raised its prices significantly above the rate of inflation and has perceived no resultant reduction in demand.’ Elsewhere, the guide stated 'Our demand forecasts point to the need for up to 11,700 new marina berths by 2015. This could be met by the creation of 47 x 250 berth marinas.’

This initiative introduced the Network Agency Agreement (NAA) which compelled new marina operators to pay the navigation authority nine per cent of mooring fees assuming 100 per cent occupancy. It also led to a policy for closure of one online mooring berth for every ten created in a new marina.

Suffice to say, by 2015 less than half the 11,700 marina berths originally projected were built. However, in many parts of the country, supply far exceeded demand leading to under occupancy. BWML has suffered along with other Marina operators in this respect. It’s occupancy rate was quoted in its last annual report as 77 per cent. This is unchanged from 2012!

Its flagship marina, Sawley, has been reported to be even worse off with one in three berths empty. On a positive note, the vast majority of its marinas are not subject to standard NAA agreement which is financially crippling some competitors.

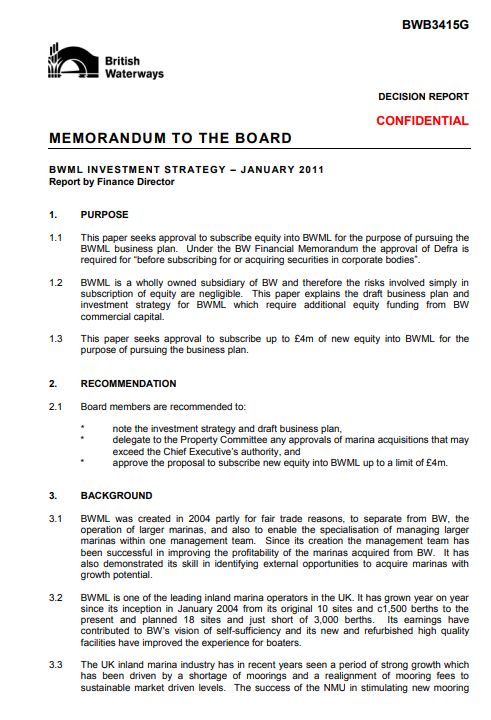

In 2011, BW Financial Director and director of BWML, Philip Ridal suggested to the BW's board that they should take advantage of competitors misfortunes. He proposed that C&RT’s investment in BWML be increased from from £6.2m by up to £4m. This extra equity was to be used to buy failing marina businesses at advantageous prices and further develop existing sites including conversion to a high proportion of residential berths. He called it 'expansion by acquisition'.

He got his wish. Indeed, C&RT invested £5m rather than £4m and now has £11.2m of investment. The policy again raised the question of anti competitive practices. In September 2011, Dominic Miles, a director of Rugby Boats Limited, queried BWML's acquisition of Portavon and Cowroast marinas using equity provided by BW without bringing the trades attention the opportunity to acquire them (Facilitating BWML marina investment).

Despite the extra equity, BWML failed to perform. MD, Derek Newton left after a significant profit slump in in 2013/14. He was replaced by Jeff Whyatt, C&RT’s South East Regional Manager. Philip Ridal quickly followed Newton by retiring. He was replaced by Sandra Kelly both as C&RT’s financial director and a director of BWML.

With BWML saying that, in its 2017/18 financial year, it will return just £250,000 to its parent, it is fairly obvious that business is in trouble yet again. £250,000 is not much of a return on C&RT’s £11.2m investment - just 2.2 per cent. It can do much better investing that money elsewhere. That’s if it can recoup its investment (or more) on selling the business.

If not then it can always up the selling price by offering the freehold of some marinas in the deal. However, the storm of protest at its attempt to sell the freehold of Blowers Green Pumphouse (Bid to sell canal pumphouse hits protests and Blowers Green U-turn by C&RT?) means that will have to tread with care.

But will it really invest the money elsewhere as its press release suggests? Probably not. One has to remember that C&RT has already borrowed significant amounts to invest. As well as an historic £13m debt inherited from British Waterways, C&RT borrowed £50m in 2016/17 using a revolving credit facility. In January this year it raised a further £100m via the issue of bonds and will raise another £50m the same way in June (C&RT to borrow £150m via bonds).

If C&RT manage to sell BWML by next Christmas, it is almost certain that the amount raised will be used to pay off the £13m Port of London Properties (POLP) debt inherited from British Waterways with must be repaid in January 2018. Why invest proceeds from the BWML sale when you would then have to sell something else to pay off the POLP debt?

Here is what C&RT say: ’All the proceeds from the sale of BWML would be invested in other income-generating assets, so as to deliver further sustainable revenue funding for maintaining the historic waterways in the Trust’s care.’

That sounds so much better than: ‘All the proceeds from the sale of BWML will go towards repaying a £13m debt to POLP (Port of London Properties)'.

Photos: (1st) BWML's current crop of marinas, (2nd) Sawley the BWML flagship, (3rd) Derek Newman at Hull Marina, (4th) Jeff Whyatt replaced Derek Newton, (5th) Philip Ridal - retired after BWML failure, (6th) Ridal's plan to acquire more marinas, (7th) Empty Berths at a BWML marina.